Are you confident in accurately reporting cryptocurrency earnings on your tax returns?

2020 is the Year of Crypto Tax Compliance

The IRS is significantly ramping up cryptocurrency tax compliance with new guidance, warning letters, and updates to tax forms. CoinTracker can help you stay compliant.

October 15, 2019 · 2 min read

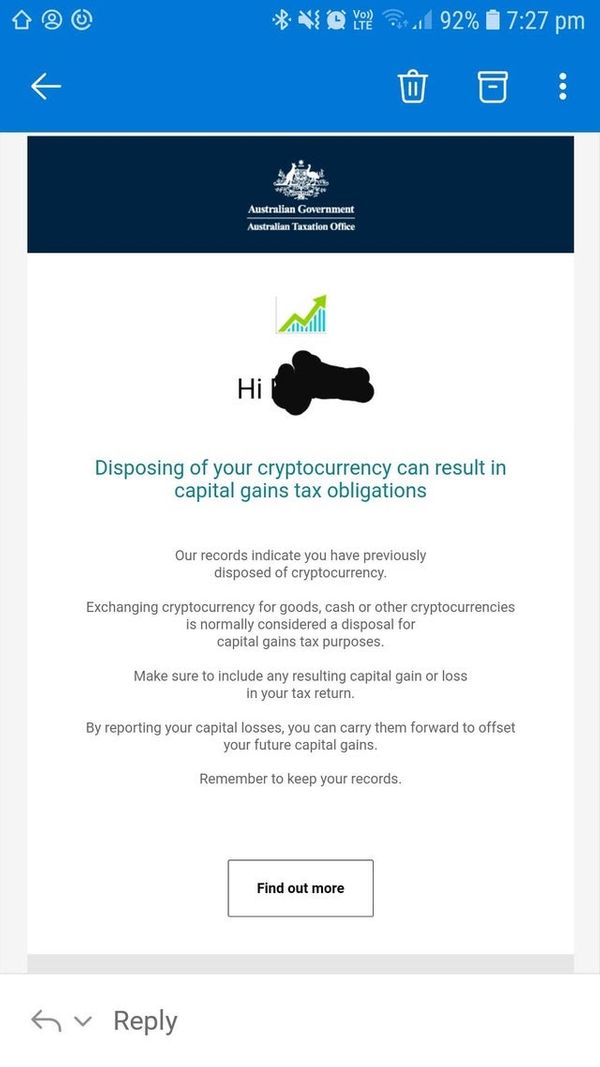

When it comes to cryptocurrency taxes, 2019 has been a very eventful year. It started in July when the IRS issued over 10,000 tax notices for taxpayers with cryptocurrency transactions. These notices came in three variations (Letter 6173, Letter 6174-A & Letter 6174).

Right after these notices, the IRS also released new major guidance: Updated FAQs & Rev. Rul 2019-24 (new crypto tax guidance explained) on crypto taxation after five years from the issuance of Notice 2014-21. This new guidance brings more clarity to the original guidance and clarifies taxation of forks, airdrops, valuation of crypto and substantiation requirements.

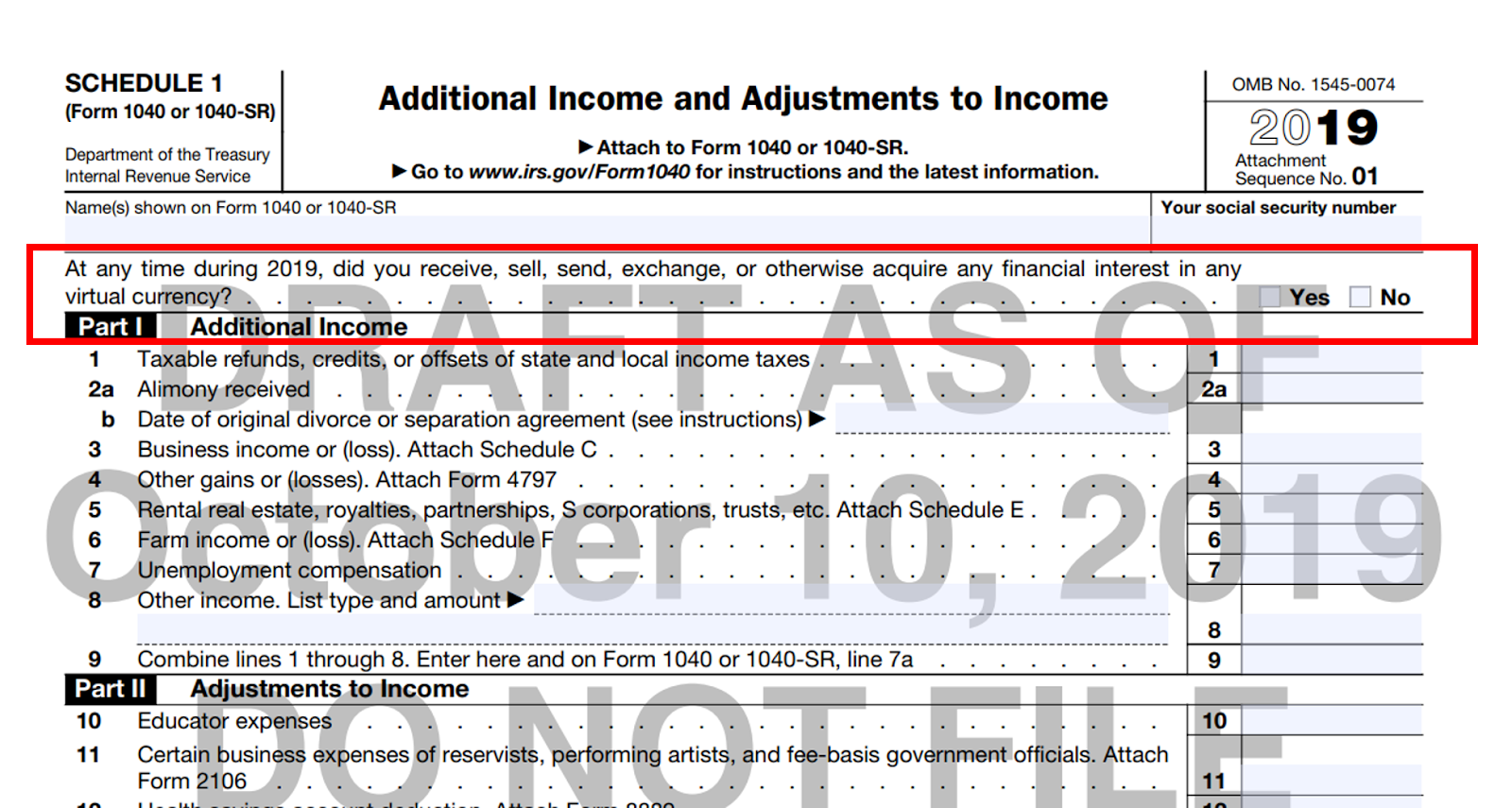

It is very clear that the IRS is actively looking into cryptocurrency related tax issues. As a part of this initiative, the IRS is also in the process of revising the 2019 Tax forms, specifically, Schedule 1, which will ask every American taxpayer:

“At any time during 2019, did you receive, sell, send, exchange, or otherwise acquire any financial interest in any virtual currency?”

What Will This Mean for Taxpayers?

The new cryptocurrency question on Schedule 1 is very broad and the IRS attempts to filter taxpayers with almost every type of cryptocurrency transactions during the tax year. Inaccurate reporting will lead to more notices and tax liabilities in the coming years. Using a tool like CoinTracker will be increasingly crucial to be compliant with the IRS.

What Will This Mean for Tax Practitioners?

Tax practitioners will need to be more cautious when preparing tax returns in 2020. As a part of the annual tax questions sent to clients via organizers, they should consider including the question on Schedule 1. This will help them identify clients with cryptocurrency transactions so they can request necessary information early. If their staff is not trained on preparing crypto taxes, this is a great time to train them as well.

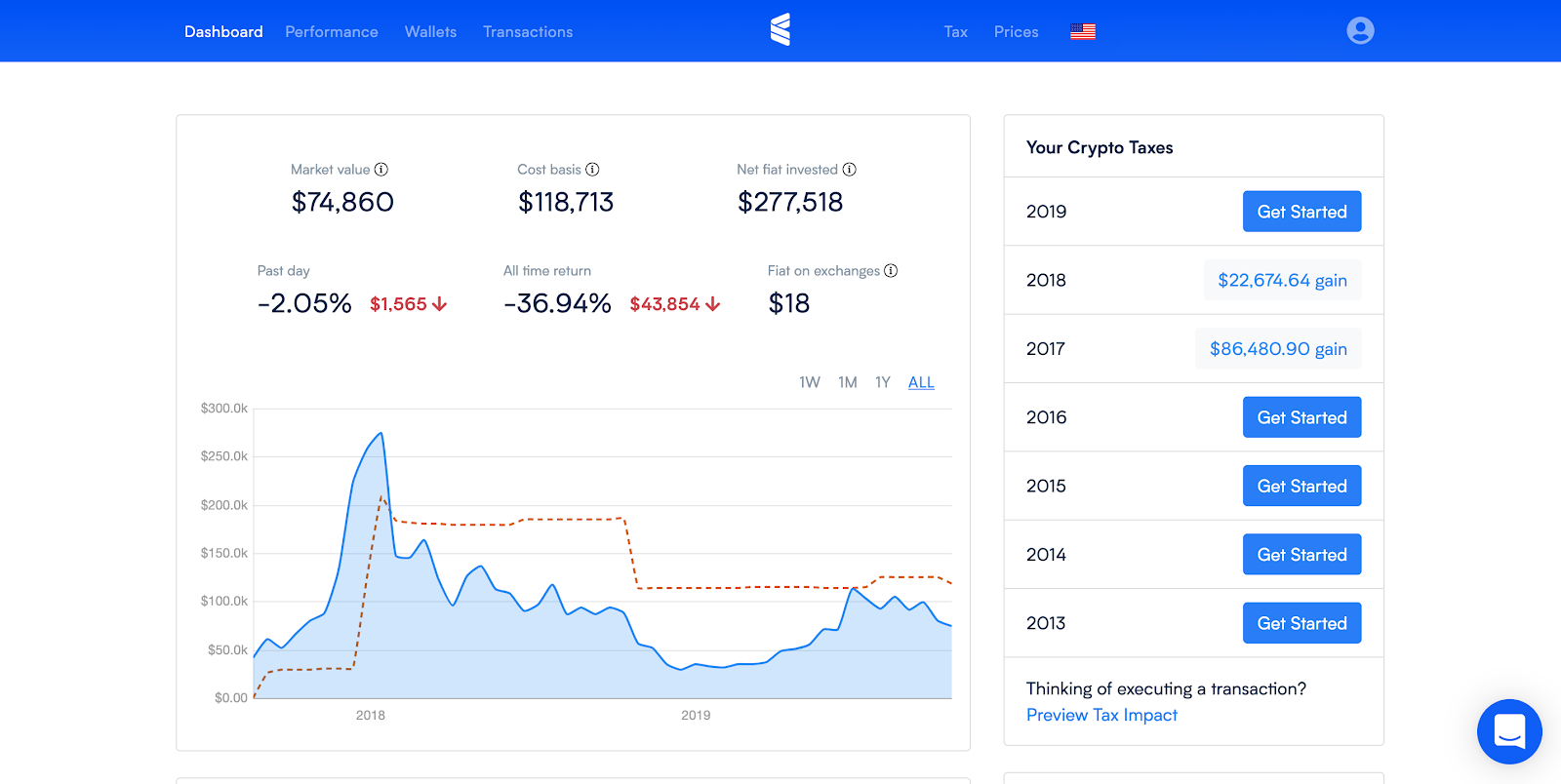

Further, tax professionals should pay attention to tools that will help them calculate clients’ cryptocurrency gains and losses. Cryptocurrency exchanges do not issue Form 1099-Bs so it is tax practitioners’ responsibility to calculate cryptocurrency related gains/losses based on client’s wallet and exchange activity. This is an extremely time consuming task and in some cases virtually impossible to perform in spreadsheets given the complexity of cryptocurrency-to-cryptocurrency trades, aidrops, forks, transfers, ICOs, coin swaps, DeFi platforms, and more. A product like CoinTracker can help accurately calculate crypto gains & losses, and produce a Schedule D and IRS Form 8949. There are also myriad other reasons accountants should pay attention to crypto taxes.

Tax law is continuously changing in the crypto space. CoinTracker is continuously monitoring the space and improving our tools to help both taxpayers and tax practitioners.

CoinTracker helps you calculate your crypto taxes by seamlessly connecting to your exchanges and wallets. Questions or comments? Reach out to us @CoinTracker

Disclaimer: this post is informational only and is not intended as tax advice. For tax advice, please consult a tax professional.