Are you confident in accurately reporting cryptocurrency earnings on your tax returns?

Five Ways to Reduce Your Crypto Tax Bill with IRS Deductions

ICO scams, tokens delistings, and exchange hacks are all frequent incidents. Luckily, the tax law allows you to deduct some of these losses.

September 20, 2019 · 5 min read

ICO scams, tokens delistings, and exchange hacks are all frequent incidents in the crypto world. For the ordinary user, these will lead to a complete or partial loss of investment. Luckily, the tax law allows you to deduct some of these losses against income to reduce hardship, subject to many complex rules and regulations. Let’s go over some types of losses described in the tax code and explore whether they can be applied to cryptocurrency losses.

Capital Losses

This is the simplest loss to claim. Per IRS notice 2014-21, cryptocurrencies are treated as property. If you sell your position at a lower price than your purchased, this will create a deductible loss that you can use to reduce your capital gains in other types of assets (e.g. stocks). If you still have more capital losses leftover than gains, you can additionally offset your ordinary income by up to $3,000 per year. Losses in excess of this amount will be rolled forward to future tax years indefinitely.

Once you connect your wallets and exchanges to your CoinTracker account, our platform calculates your capital/ordinary losses and generates Form 8949 and Schedule D.

Non-business Bad Debt Loss Deduction

Your personal cryptocurrency lent to a DeFi platform that is not recoverable due to the platform being shut down or a scam may be deducted as non-business bad debt. Non-business bad debts must be totally worthless to be deductible. You cannot deduct a partially worthless nonbusiness bad debt. Note that unrecoverable investments in Initial Coin Offerings (ICOs) cannot be deducted under this provision because this provision applies only to debt instruments. Investments in Initial Coin Offerings are generally considered to be investments in equity rather than debt.

You can report a non-business bad debt as a short-term capital loss on Form 8949, Sales and Other Dispositions of Capital Assets (PDF), Part 1, line 1. Enter the name of the debtor and "bad debt statement attached" in column (a). Enter your basis in the bad debt in column (e) and enter zero in column (d). Use a separate line for each bad debt. It’s subject to the capital loss limitations described above. A non-business bad debt deduction requires a separate detailed statement attached to your return. The statement must contain: a description of the debt, including the amount and the date it became due; the name of the debtor, and any business or family relationship between you and the debtor; the efforts you made to collect the debt; and why you decided the debt was worthless.

Sample Statement

The taxpayer loaned $XX,XXX to <name of the platform> on MM/DD/YYYY. The loan amount was due on MM/DD/YYYY as outlined in the agreement attached. The taxpayer has no business or family relationship with the platform mentioned above. The taxpayer has made all reasonable efforts to collect this debt. These include emailing multiple times to the platform, reaching out to customer service, etc. Unfortunately, none of these attempts have been successful so far. According to several online sources, this platform is fraudulent and has disappeared without leaving any trace. Attached are some news relevant to the platform. Consequently, this debt is deemed to be non-business bad debt.

Casualty & Theft Losses

Stolen/hacked wallets & exchanges, lost access to private keys, sending crypto to the wrong address and loss of funds due to negligent acts are some examples for casualty and theft losses. Casualty & Theft losses are governed by §165 of the IRS code and further explained by related regulations.

Prior to January 1st, 2018, individual taxpayers were generally allowed to claim an itemized deduction for uncompensated personal casualty losses, including those arising from fire, storm, shipwreck, or other casualty, or from theft. Under this regime, personal casualty or theft losses were only deductible to the extent they exceeded $100 per casualty or theft event. In addition, the aggregate net casualty and theft losses for the year were deductible by those who itemized their deductions but only to the extent that the loss exceeded 10% of an individual's adjusted gross income (AGI).

However, for tax years 2018 through 2025, if you are an individual, casualty and theft losses of personal-use property are deductible only if the losses are attributable to a federally declared disaster (federal casualty loss). Therefore, in most cases, funds lost due to stolen or hacked wallets are not a deductible loss in the tax return.

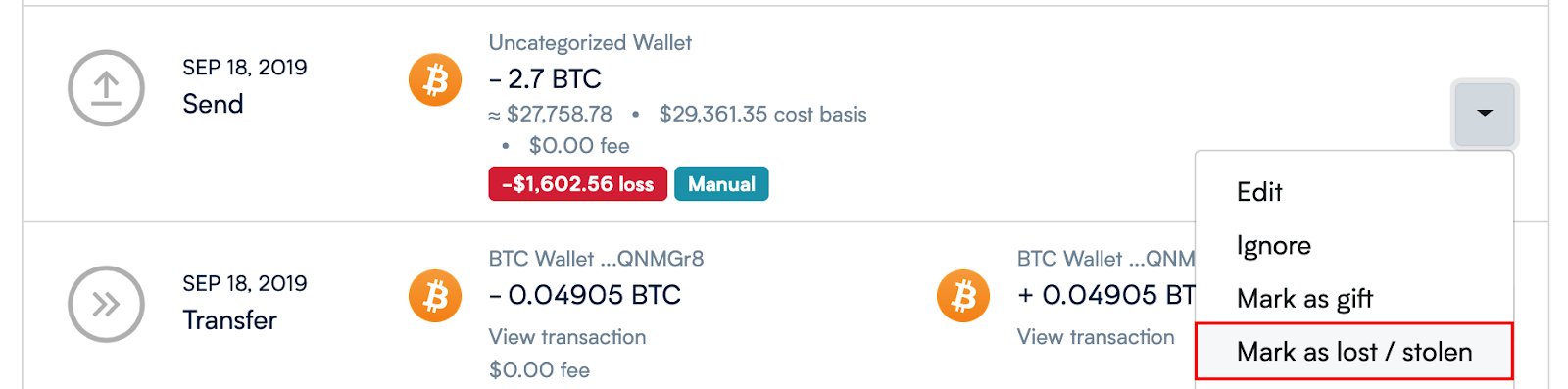

If deductible, you can manually edit a sent transaction in CoinTracker to be a trade for $0.00000001 which will show a 100% capital loss for the coins in question (example below).

If it is past January 1st, 2018, you can mark the sent coins as lost/stolen from the dropdown on the transactions page. This will remove the coins from your portfolio without triggering a capital gain/loss event.

Ponzi Scheme Loss

Generally, losses related to Ponzi schemes are governed by Rev. Proc 2009-20 (as modified by Rev. Proc. 2011-58). Ponzi scheme losses are reported on Section C of IRS Form 4684. Qualified ponzi scheme losses arise from “a specified fraudulent arrangement for which authorities have charged the lead figure by indictment, information, or criminal complaint with a crime”. Note that schemes like Bitcoinnect (BCC) are often referred to as “ponzi schemes” in general media. However, these do not meet the IRS definition of a ponzi scheme because often times authorities are unable to file a criminal complaint due to the distributed nature of the business. Therefore, if you lose your investment in a “ponzi-like” scheme, that loss is unfortunately not deductible as a Ponzi Scheme loss (this may be deducted as a regular theft loss if it occured and discovered prior to January 1, 2018 as mentioned above).

Worthless Security Loss Deduction

As the name suggests, worthless securities have a market value of zero. Worthless securities can include stocks or bonds that are either publicly traded or privately held. These securities, along with any securities that an investor has abandoned result in a capital loss for the taxpayer and can be claimed as such when filing taxes.

Note: these are only applicable to “securities” per IRS §165(g).

Bitcoin is not classified as a security. Ethereum is also likely not a security. Some long tail ICO tokens or Security Token Offerings (STOs) may be classified as securities for which this deduction could apply, but it would not apply to most larger cryptocurrencies.

In conclusion, you may feel like you are eligible for a tax write-off because your wallet got hacked or involved in a scam. However, the deductibility of these losses are subject to complex rules set by the IRS. Since there is no detailed guidance on crypto, we encourage you to take the most conservative approach on claiming losses to mitigate your chances of getting audited.

CoinTracker helps you calculate your crypto taxes by seamlessly connecting to your exchanges and wallets. Questions or comments? Reach out to us @CoinTracker.

Disclaimer: this post is informational only and is not intended as tax advice. For tax advice, please consult a tax professional.