Are you confident in accurately reporting cryptocurrency earnings on your tax returns?

2024 Crypto Tax Loss Harvesting Guide

A loophole in the tax code allows the savvy investor to lower their bill with crypto tax loss harvesting. CoinTracker has the tools you need.

February 9, 2024 · 3 min read

tl;dr — CoinTracker assists you in reducing your tax bill with our Tax Loss Harvesting Tool (available with a Prime or Ultra subscription plan)

As you may have seen in CoinTracker's 2024 Crypto Tax Guide, for most people, the largest expense over the course of a year is not their rent, housing, car payment, or food. It’s their tax bill.

Tax loss harvesting is a compelling form of tax planning that allows people to offset their tax expenses by selling assets at a loss before the end of the calendar year. When it comes to cryptocurrency, it’s a low-effort way to sometimes save tens of thousands of dollars in under an hour, all while maintaining your existing portfolio.

How to Harvest Crypto Tax Losses?

Let’s say Max saw the price of bitcoin climbing. He purchased 1 bitcoin (BTC) near the top of the market at $62,000 in November 2021. Two years later (November 2023), BTC is trading at $39,000, so Max now has the opportunity to tax loss harvest $23,000 worth of unrealized capital losses.

Here’s how tax loss harvesting works for crypto:

- Cost basis: $62,000 (price Max bought his bitcoin)

- Fair market value: $39,000 (price of bitcoin at that time)

- Harvestable losses: $23,000 (difference between the two)

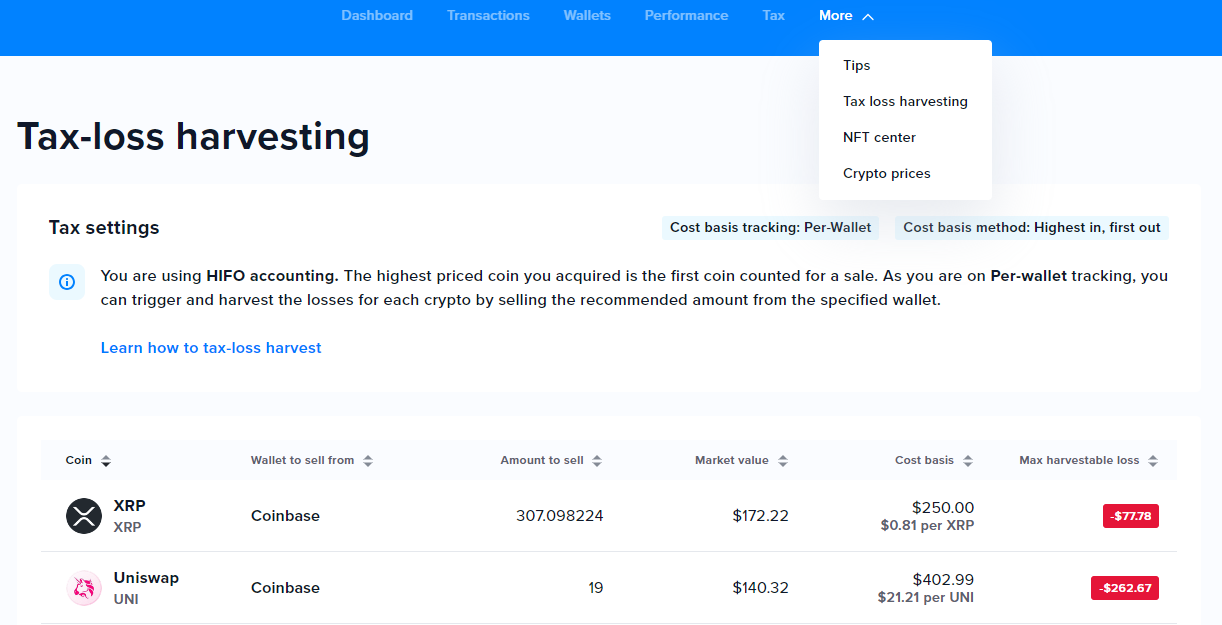

To harvest the losses, Max needs to dispose of his bitcoin before the end of the tax year (e.g. December 31 in the US). CoinTracker makes this simple with our Tax Loss Harvesting Tool (available with a Prime or Ultra subscription plan). This tool tells users which assets they can tax loss harvest, the wallet the asset is held, the amount to sell, and estimates the maximum loss. (Make sure you resolve any needs review items first or these amounts could be inaccurate.)

Note: Tax-loss harvesting is disallowed in Canada, UK, and some other countries without waiting for a 30-day period after an asset is sold to be re-purchased. In Australia, the ATO has warned against tax loss harvesting without honoring wash sales.

When Should You Tax Loss Harvest Cryptocurrency?

Anytime that the market value of your asset drops beneath its cost basis, there is an opportunity to tax loss harvest and effectively save money on your next crypto tax bill.

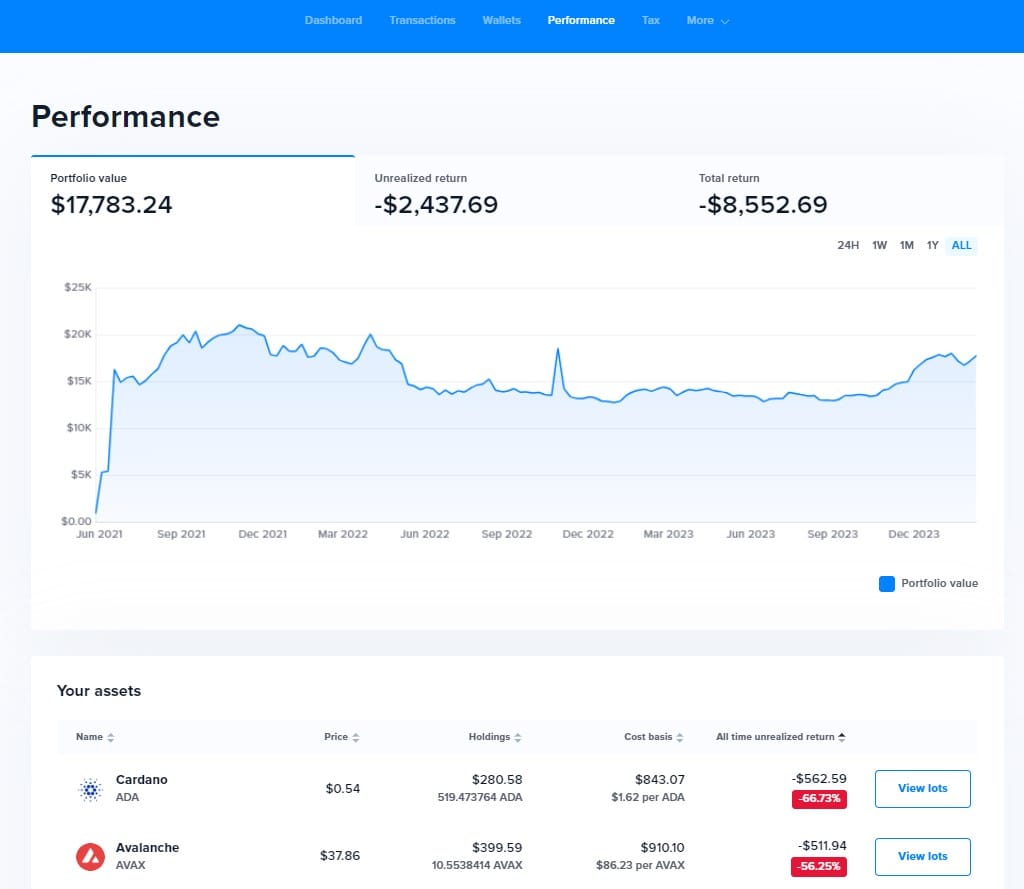

CoinTracker makes this easy for you on the Performance page by visualizing your unrealized performance; anytime the all time unrealized return is red (cost basis exceeds the holdings value), you have an opportunity to tax loss harvest.

There are a few simple steps to tax loss harvest your cryptocurrency:

- Identify the crypto assets you hold at a harvestable loss (available on the CoinTracker tax loss harvesting dashboard)

- Sell the amount of that asset (can be for fiat, a stablecoin, or any other cryptocurrency)

- Assuming you would like to maintain the same composition of your portfolio as before, repurchase the same amount of the asset

- Transfer your assets back to the wallets in which you would like to hold your assets long term

- Sync your CoinTracker dashboard from the wallets page

Wash Sales and Cryptocurrency

In the U.S. the IRS has a wash sale rule for securities. It does not apply to Bitcoin since it is not a security, but may apply to other crypto assets that the SEC deems securities. To be extra safe, you can avoid purchasing back the same asset for 30 days if you are not sure if it is a security or not.

In plain English, when you tax loss harvest stocks, you have to wait 30 days to re-purchase anything you sold (in order to claim the loss on your taxes), but this does not apply to any cryptocurrencies that are not securities, such as Bitcoin and Ethereum. This means that you can sell your crypto and instantly buy it back, maintaining the same position you had before while claiming a tax loss. That’s a win-win.

Note: Tax Loss Harvesting must be done before the end of the tax year, which in the United States is December 31. Individual tax lots within a particular coin can have different cost bases, so please ensure you are considering the taxable implications of each trade before executing it. If you are unsure, you can manually add the trade in CoinTracker to see what happens before you actually make the trade.

If you have any questions or comments about crypto taxes, let us know on X @CoinTracker.

CoinTracker integrates with 300+ cryptocurrency exchanges, 8,000+ cryptocurrencies, and makes crypto tax calculations and portfolio tracking simple.

Disclaimer: This post is informational only and is not intended as tax advice. For tax advice, please consult a tax professional.